If secondary markets facilitate NFTs’ selling and buying, NFTFi enhances them by integrating DeFi primitives. Besides money markets (lending and borrowing), NFTFi protocols also span spot-DEXs, Perpetual DEXs (Perp-DEXs), options, and many more. And each serves one of these premises: improving NFT trading and expanding NFTs’ productivity.

Money markets

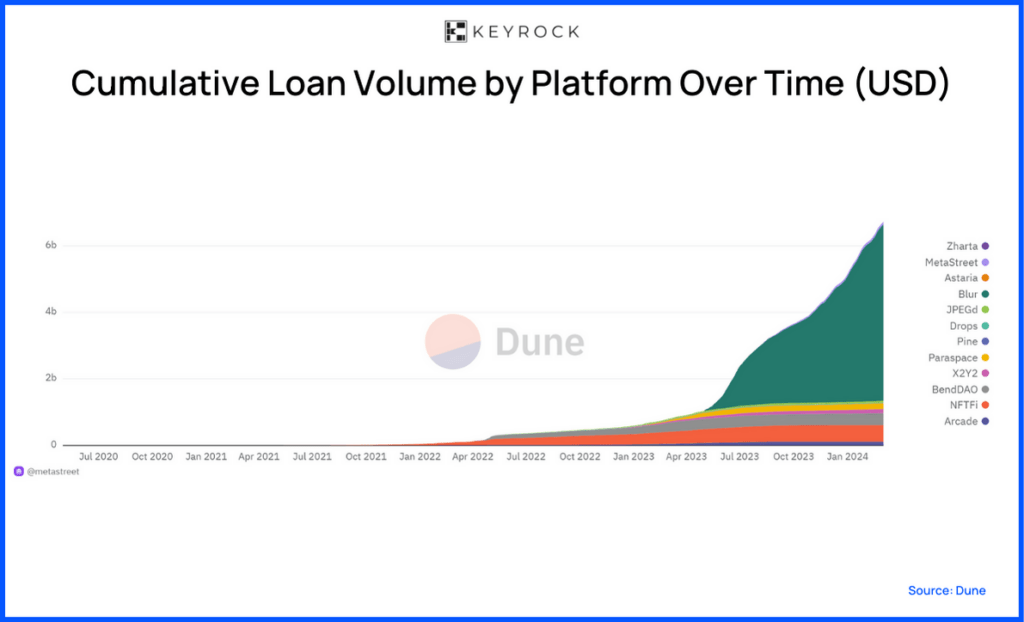

Probably one of NFTFi’s most important and disruptive value propositions. A money market allows you to use your NFT as collateral to borrow another asset, such as ETH. This means that NFT owners can access liquidity without selling their NFTs.

But it doesn’t stop there. Investors can lend assets such as ETH against an NFT, thereby generating a yield on their holdings. In essence, the money market presents a robust use case for both lenders and borrowers.

NFT collateralisation is just one solution that has emerged to broaden NFT utility and unlock holding’s liquidity. But just as in any market, price volatility is a risk factor to tame to guarantee liquidity flow. And having big actors with ample capital entering these markets could bring lending-borrowing to the next level.

Market makers play a pivotal role in enhancing the liquidity of money markets, notably by underwriting loans against NFTs. Our efforts in the Solana lending markets have significantly contributed to this, with over 80 collections and $7 million in underwriting, on protocols such as Sharky.fi. Making markets more efficient on these platforms. And we’re fully committed to doing so.

This commitment extends to Bitcoin ordinals on Liquidium, featuring collections like Runestones and Nodemonkes. In the EVM space, our focus lies on generative art NFTs. We have provided loans for artwork such as Fidenza and Squiggle working with platforms like Gondi, Cyan, NFTFi, and Zharta.

Fidenza #159. One of Keyrock’s lending markets on Gondi.

These platforms offer interesting loan features, which, as market makers, allow us more room to adjust loan structures. Gondi’s refinancing feature is one good example. They enable active loan refinancing for lenders and offer negotiation via smart contracts without borrower intervention required.

Spot-DEXs

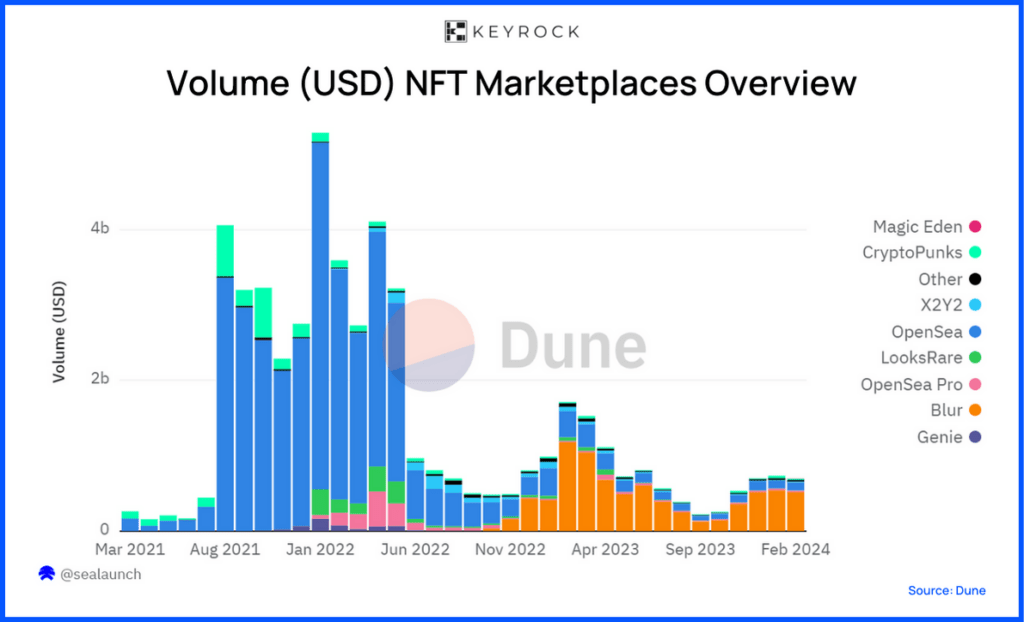

Traditionally, NFTs have been traded on dedicated marketplaces such as OpenSea, Blur, and LooksRare. These platforms function similarly to eBay, serving as P2P marketplaces where sellers list assets at prices they consider fair, leaving buyers to determine their value.

This model, however, complicates the price agreement process between buyers and sellers. Spot-AMMs, exemplified by SudoSwap, employ a pricing algorithm–a bonding curve–to simplify this. Liquidity Providers deposit assets, enabling the buying and selling of NFTs based on the bonding curve. This mechanism is just an example of how different AMMs enhance the trading experience by facilitating trading against the liquidity pool.

As market makers, we are very familiar with spot markets. By tweaking our algorithms from traditional spot-DEX order books to these NFT platforms, it was a logical decision for us to begin experimenting in these markets. We discovered that market making on platforms like Blur and Mintify is quite similar to how we conduct spot trading.

Derivatives

Derivative protocols like Perp-DEXs or Options-DEXs allow investors to speculate on NFT values without direct ownership and hedge downside risk.

NFTPerp is a notable example of utilising a virtual AMM (vAMM). The vAMM processes trades through a smart contract vault, which holds all traders’ collateral for a given asset. In this setup, profits and losses are directly transferred between traders, enabling positions to be taken on NFT values without actual ownership.

Market makers use derivatives markets to trade, hedge their exposure, or actively engage in market making. Our interest particularly lies with NFT options. This is a relatively new market, and we’re actively engaging with multiple platforms, such as Wasabi on Blast and Tensor Trading, Magic Eden, and Sharky.fi on Solana.