While there are different kinds of fees associated with trading on-chain, such as gas fees, trading fees, or front-end fees, we’re going to focus on trading fees that are fully accrued by LPs.

Uniswap’s fees comprise LP Fees or Swap Fees, paid by traders and accrued by LPs. Uniswap Labs charges a front-end fee for those trading directly through its interface. Finally, Protocol Fees, or the fee switch, divert a portion of LP Fees back to Uniswap itself.

Note that Uniswap Labs is a commercial company, and Uniswap Foundation is a non-profit that focuses on governance and community.

LP Fees or Swap Fee

Every trade on Uniswap incurs a fee. Fees are distributed pro-rata among LPs in a pool.

V1: An LP fee of 0.30% was taken out on each trade and added to the pool’s reserves.

V2: The protocol still applied a 0.30% fee to trades.

V3: Uniswap v3 introduced multiple pools for each token pair, each with different fee tiers. Liquidity providers can create pools at three fee levels: 0.05%, 0.30%, and 1%.

V4: Fee tiers no longer need to be limited thanks to the new hook functionality and the creation of a singleton architecture. Pool creators can set them to the rate they deem the most competitive or personalise them with a dynamic fee hook.

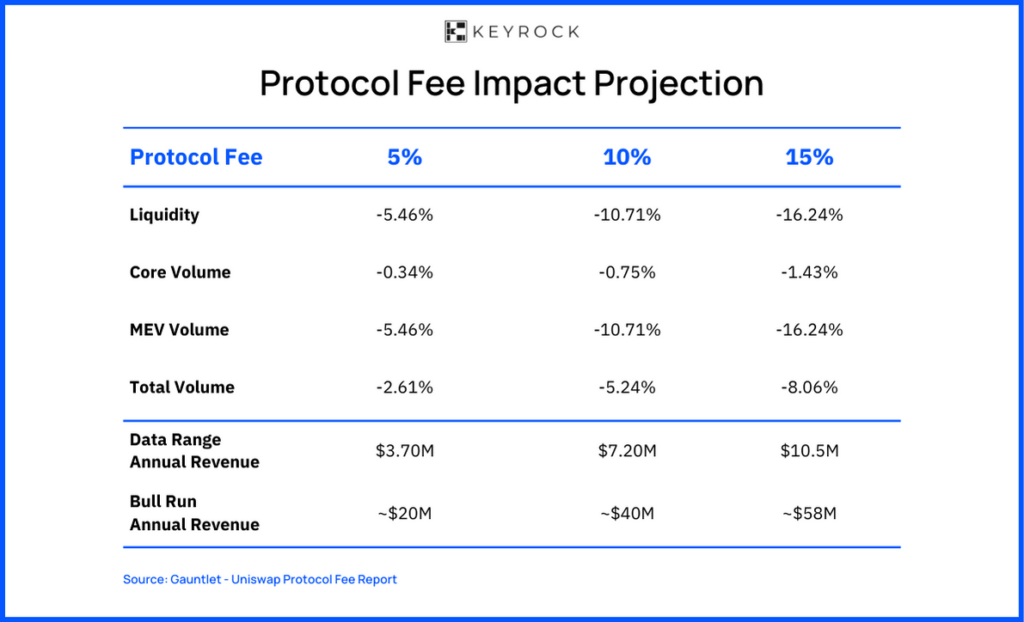

Protocol Fees

Introduced in V2, the “fee switch” mechanism allows a portion of LP fees to be redirected. Fees could be diverted to the protocol’s treasury controlled or potentially to $UNI holders.

In Uniswap V2, the protocol fee rate was fixed at 0.05%, which would be subtracted from the 0.30% LP swap fee, leaving liquidity providers with a 0.25% fee they can redeem.

This feature is deactivated by default and requires consensus from $UNI governance to activate the fee switch. This consensus has not been reached yet.

Uniswap V3 offers more flexibility, allowing governance to set the fee. The protocol fee can be set as 0 or between one-fourth and one-tenth. This value is set at a pool level, so each pool can have an independent protocol fee.

There have been various proposals regarding its activation and rate for Uniswap V3, but a consensus has yet to be reached.

Front-end Fee

On October 18, 2023, Uniswap Labs implemented a 0.15% swap fee on specific tokens to swaps conducted through its main interface. This move aimed to generate revenue to support operations, including research, development, and the expansion of Uniswap’s platform and ecosystem.

Since implementing the fee, Uniswap Labs has gained $3.5 million in revenue over 100 days, projecting an annual revenue of $13.02 million, despite only 1% of Uniswap’s volume incurring these fees. The minimal impact on trading volumes makes it challenging to assess the overall impact of this fee. For more detailed insights into the front-end fee, see Dune Dashboard.