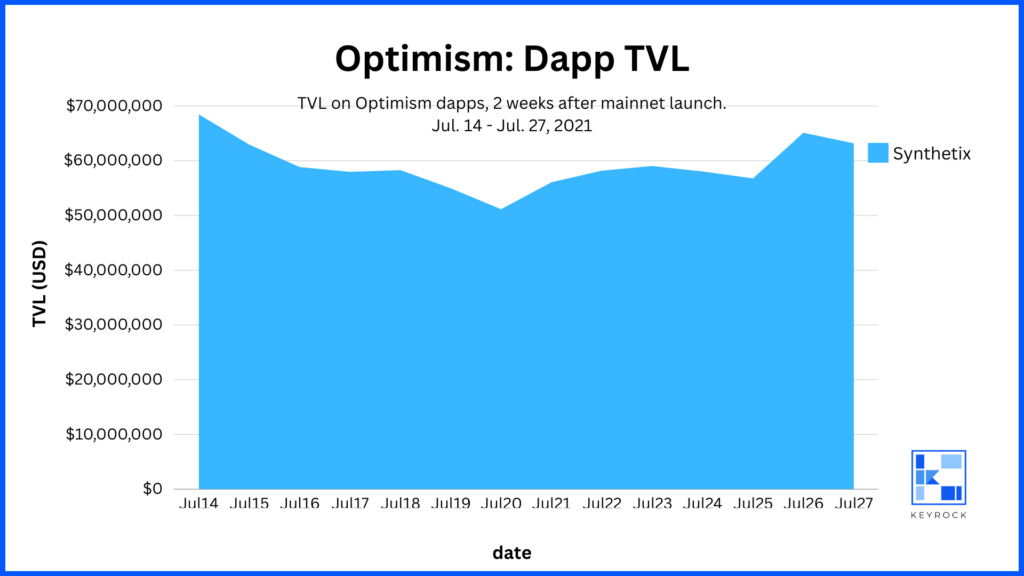

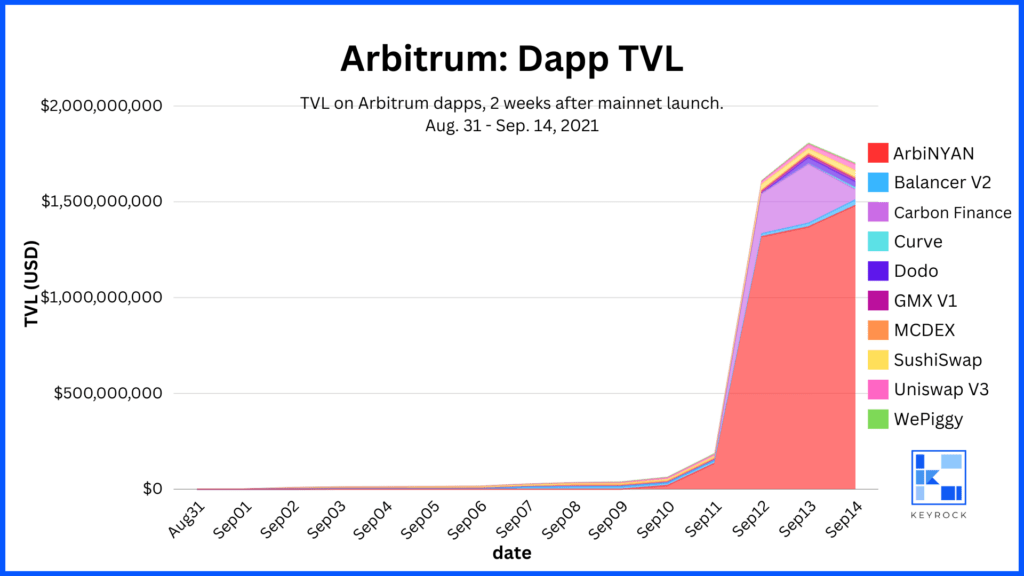

We observed app TVL during the first 2 weeks after the Arbitrum One mainnet launch on August 31, 2021.

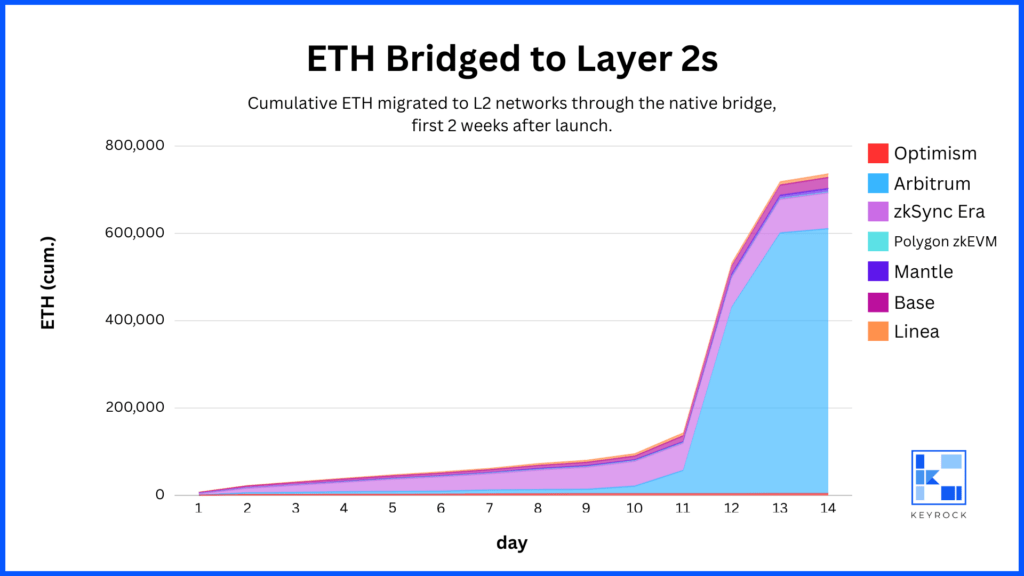

Despite launching on August 31, it wasn’t until September 11th that the data shows a significant increase in TVL among Arbitrum applications. This app activity aligns with our original observation from our first ETH migration analysis, showing that Arbitrum experienced a huge influx of ETH from Ethereum at the same time.

On September 11, 180,000 ETH was deposited to Arbitrum in less than one hour, nearly doubling the total amount of ETH bridged to Arbitrum at that time to 360,000. By September 12, nearly 600,000 ETH had been deposited to the Arbitrum mainnet from Ethereum.

In our ETH migration analysis, we did not conclude what drove the significant uptick in bridged ETH. Looking at app TVL data, however, reveals the motivation behind the huge deposit of ETH onto the Arbitrum mainnet on September 11: ArbiNYAN.

ArbiNYAN was a memecoin liquidity mining scheme that exploded onto the scene in September 2021. It was the first native Arbitrum application to attract major attention. Just as BALD had done for Base in 2023, ArbiNYAN launched Arbitrum into a web3 frenzy.

On September 10, the TVL across the top 10 apps on Arbitrum was $61,929,474 USD. ArbiNYAN was responsible for 31% of that TVL ($19.34MM). By September 12, Arbitrum’s TVL among the top 10 apps had skyrocketed to $1,609,246,339 USD — a 2,500% increase in 48 hours. By that time, ArbiNYAN was responsible for 82% of that TVL ($1.31bn USD).

To state it differently, on September 12, ArbiNYAN’s TVL alone was 21x larger than the TVL of the entire Arbitrum network just 2 days prior.