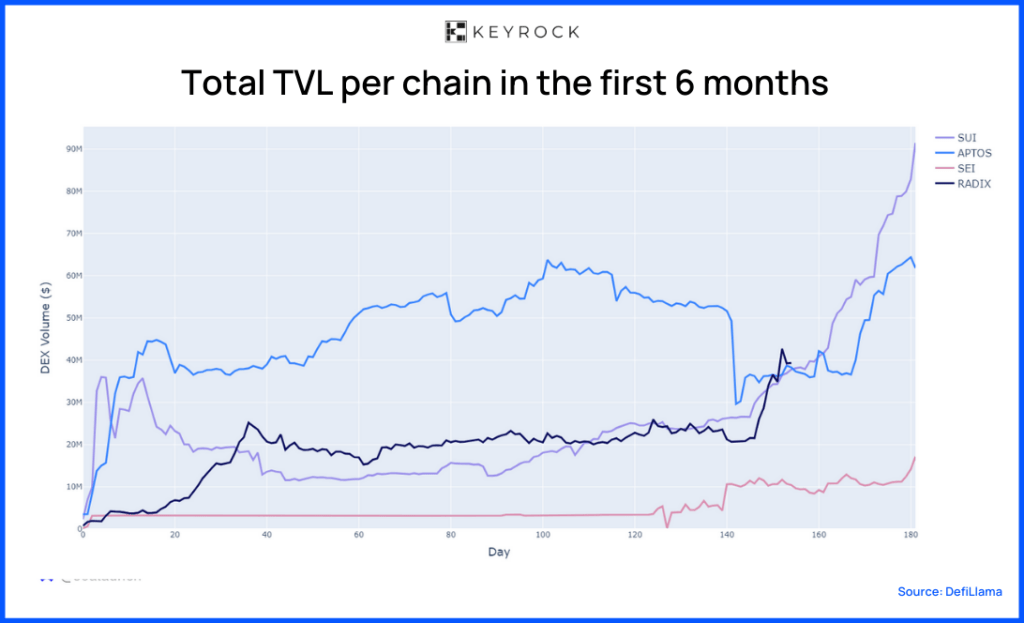

We’ve mapped the terrain of all ecosystems. Let’s analyse each of them independently. Here, we’ll look into the following metrics/charts: TVL by protocol, TVL by category, and DEXs volumes.

SUI – Analysis

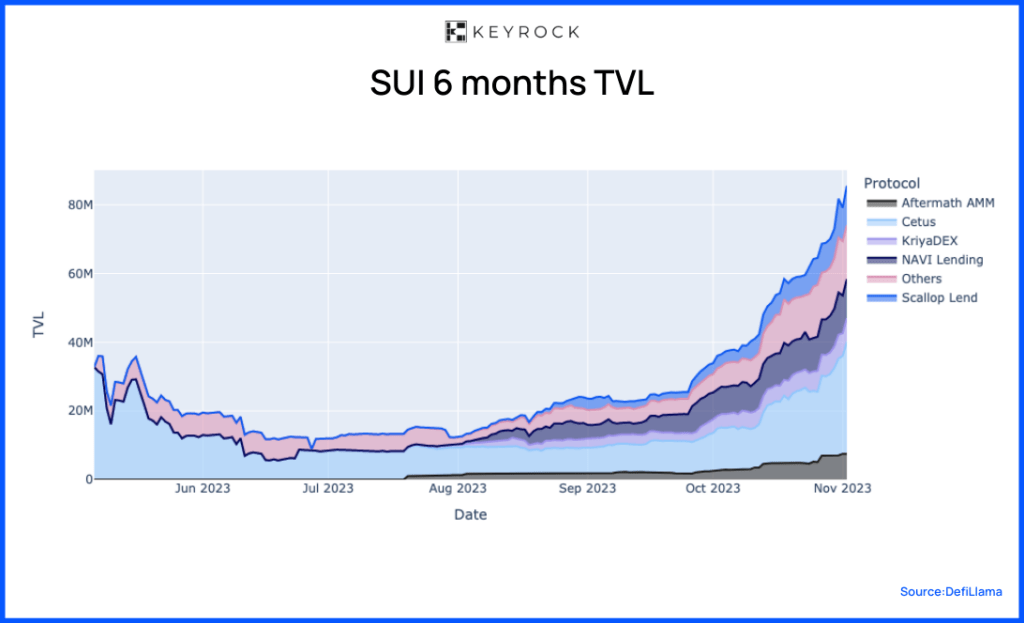

SUI, launched in May 2023, stabilised a TVL of around $20 million during the first four months, later surging to $80 million.

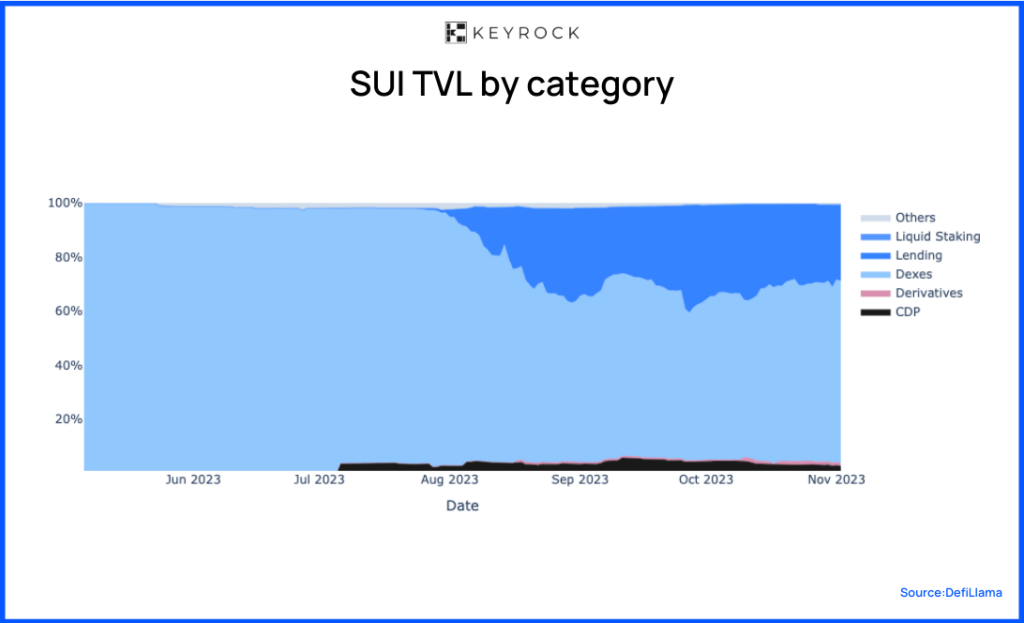

DEXs, spearheaded by Aftermath AMM, CETUS, and Kriya DEX, initially led the chain’s activity. Over time, lending protocols such as NAVI Lending and Scallop Lend began to carve out their dominance, significantly contributing to the chain’s TVL increase.

Though CDP-based stablecoins and derivative protocols piqued interest, their TVLs paled compared to DEXs and lending protocols.

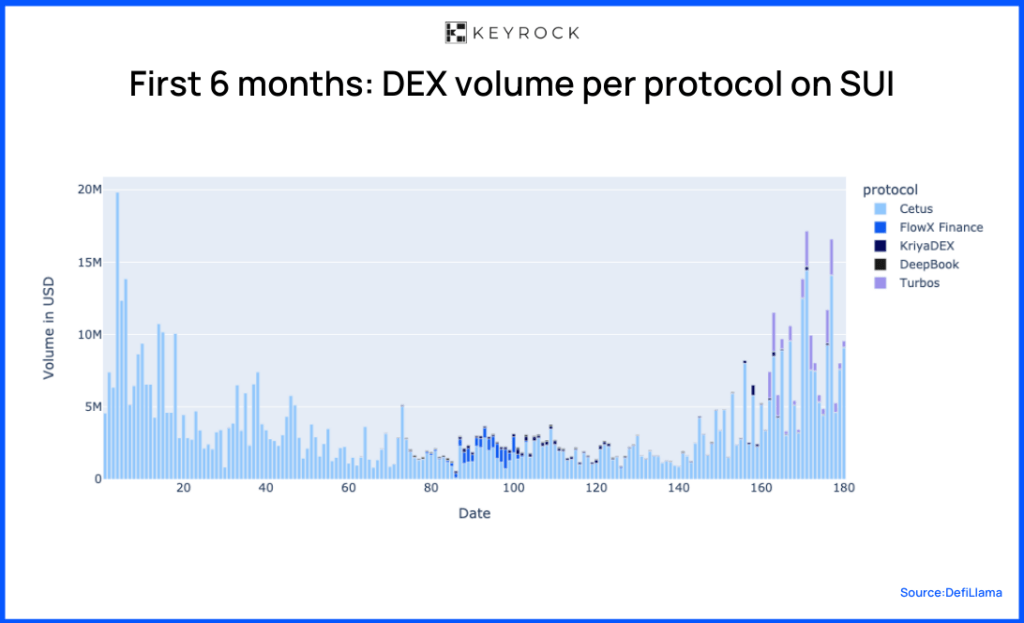

At launch, trading volume surged, peaking at $20 million approximately five days later. Over the initial four months, this figure gradually declined. However, as TVL increased in October 2023, DEX volumes experienced a significant uptick—from an average of $2.5 million daily to $17.5 million. Cetus emerged as the dominant DEX, capturing the majority of this volume.

Aptos – Analysis

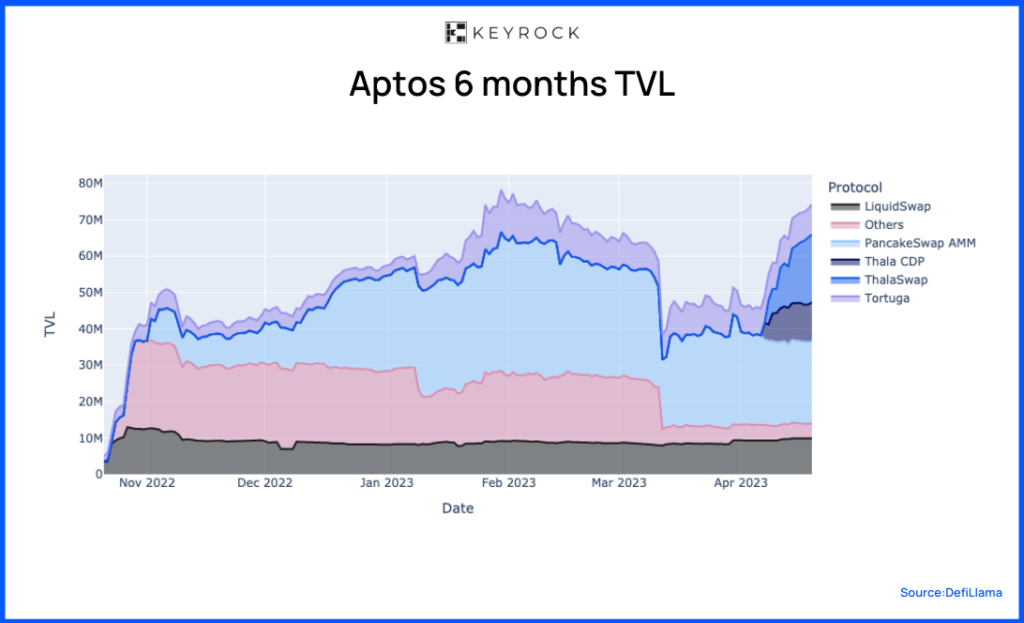

Despite its debut during a bear market, Aptos swiftly garnered attention, securing over $40 million and climaxing at $75 million by the close of our snapshot.

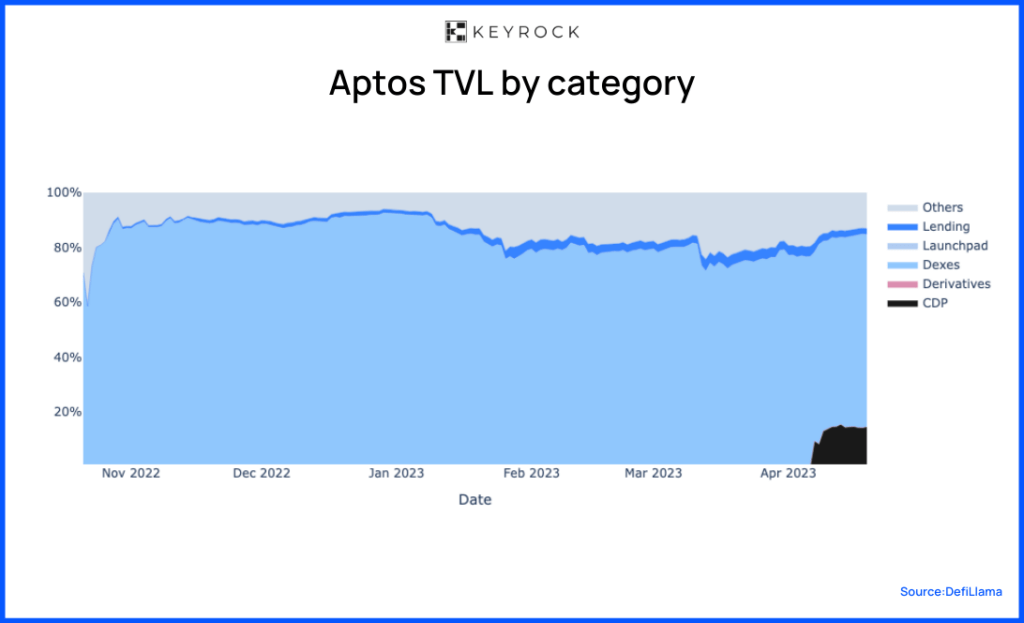

DEXs, notably Liquidswap, PancakeSwap, and ThalaSwap, dominated the chain’s TVL, accounting for 60% to 80%. Hot on their heels, liquid staking protocols like Tortuga and Thala CDP gained traction as the snapshot period ended. Meanwhile, derivatives, lending, and launchpads played more marginal roles in the TVL landscape.

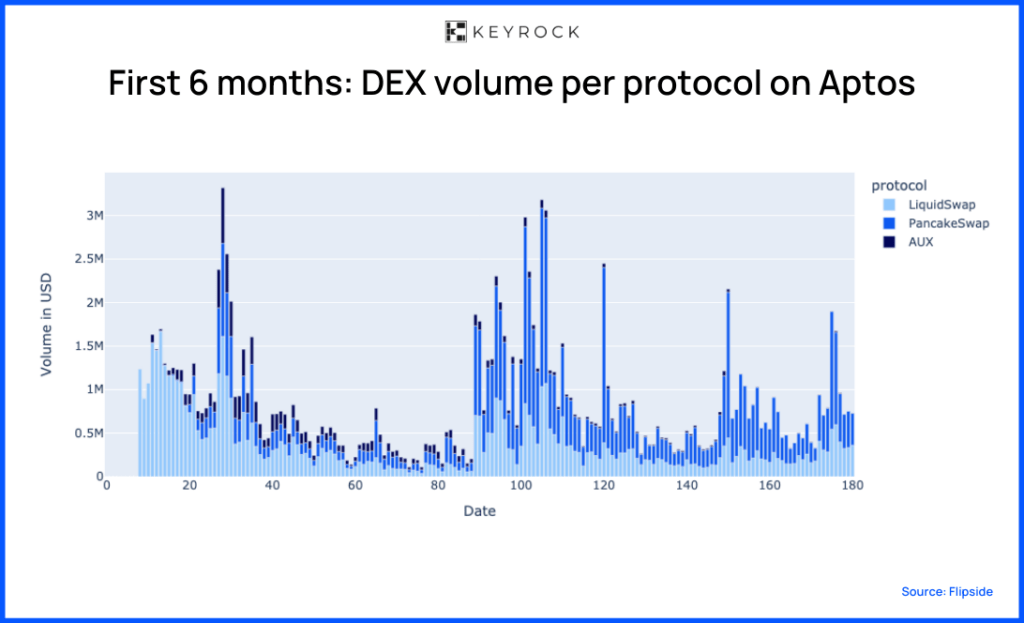

Note: Data is solely on the APT/USDC pool as a proxy to facilitate comparison across exchanges, given that APT/USDC is the most liquid pair on the exchanges.

Activity was pretty high during the first 2 months. Coincidentally, a period of very low activity occurred during the FTX blowup. Despite Liquidswap boasting approximately $10 million in liquidity, daily trading volumes hovered between $500k and $1m.

This trend reversed in early January, with volumes and activity surging and remaining somewhat stable until the end of the snapshot. Most of this volume occurred on Pancakeswap, likely because it’s the DEX with the most liquidity.

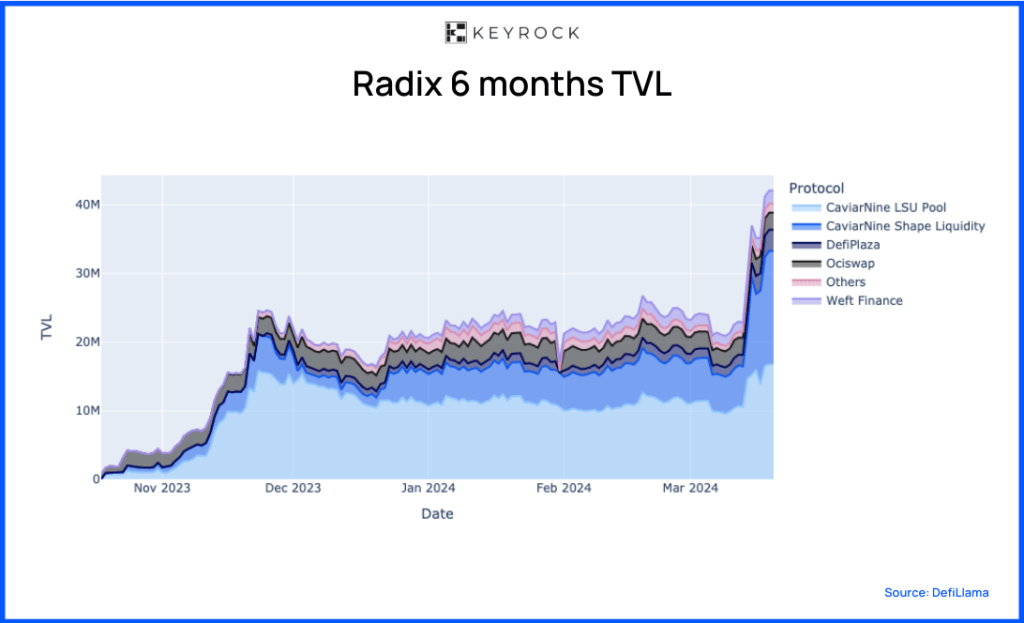

Radix – Analysis

Radix made steady progress toward $25 million from its inception. It hit the $25m mark approximately 30 days after launch. Over the following three months, its Total Value Locked (TVL) remained stable. Having launched in October 2023, our analysis is based on four months of data.

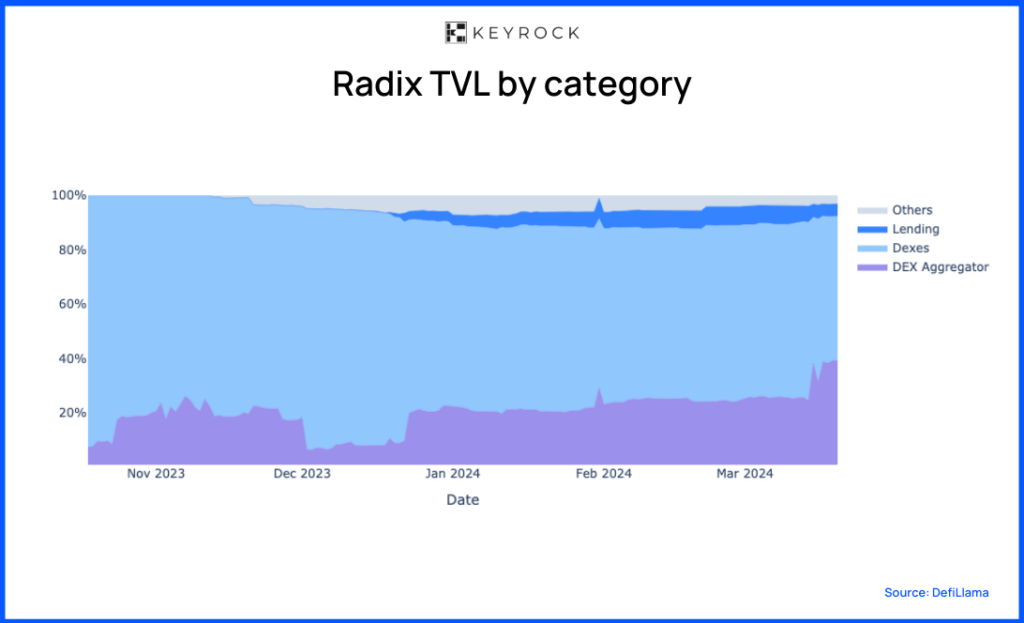

DEXs and DEX Aggregators, such as CaviarNine and DefiPlaza, spearheaded the chain’s TVL, contributing between 80% and 100% of its total. Though still emerging on Radix, lending is predominantly offered by Weft Finance, accounting for less than 5% of the TVL.

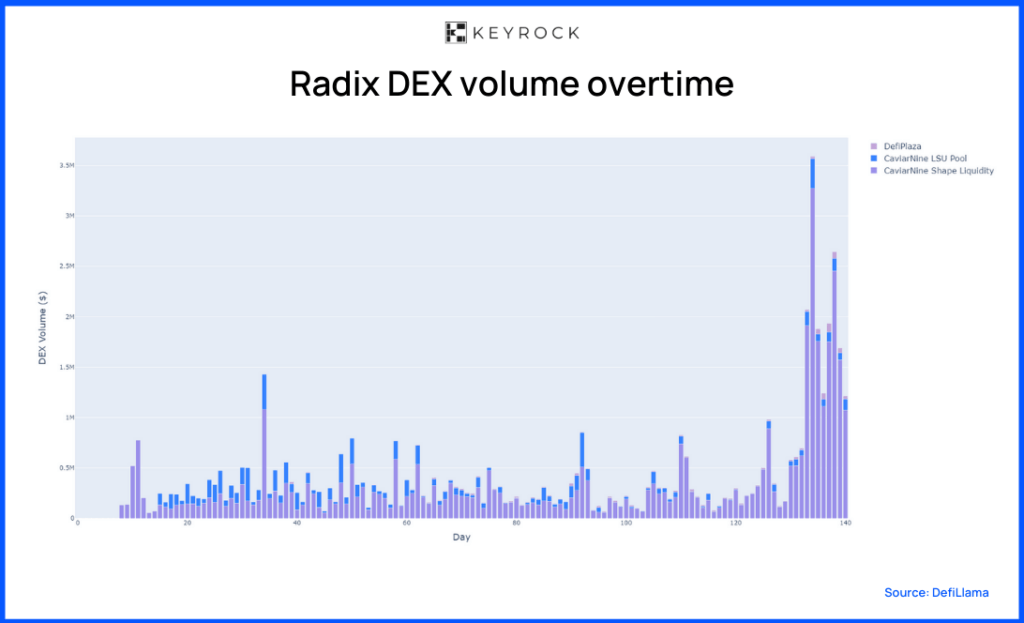

Radix achieved a TVL of $25 million, but the DEX activity remained subdued in the initial months. The average daily volume fell below $400k. Like other chains, DEX activity picked up towards the end of the snapshot, and roughly $1 million to $3.5 million were traded daily. Caviarnine, with both the LSU and Shape Liquidity, took the lead on Radix’s ecosystem.

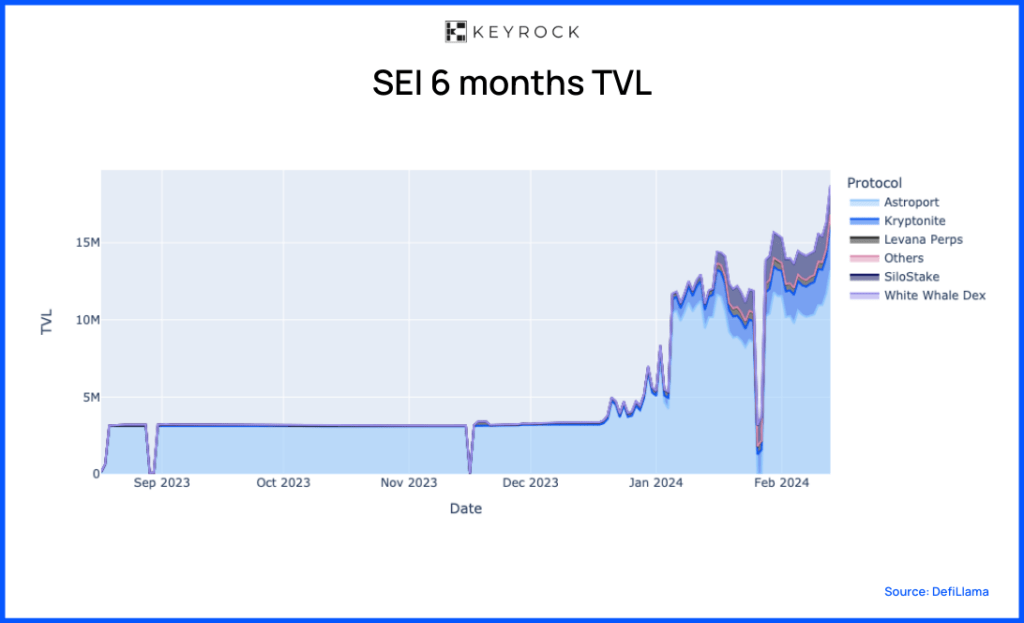

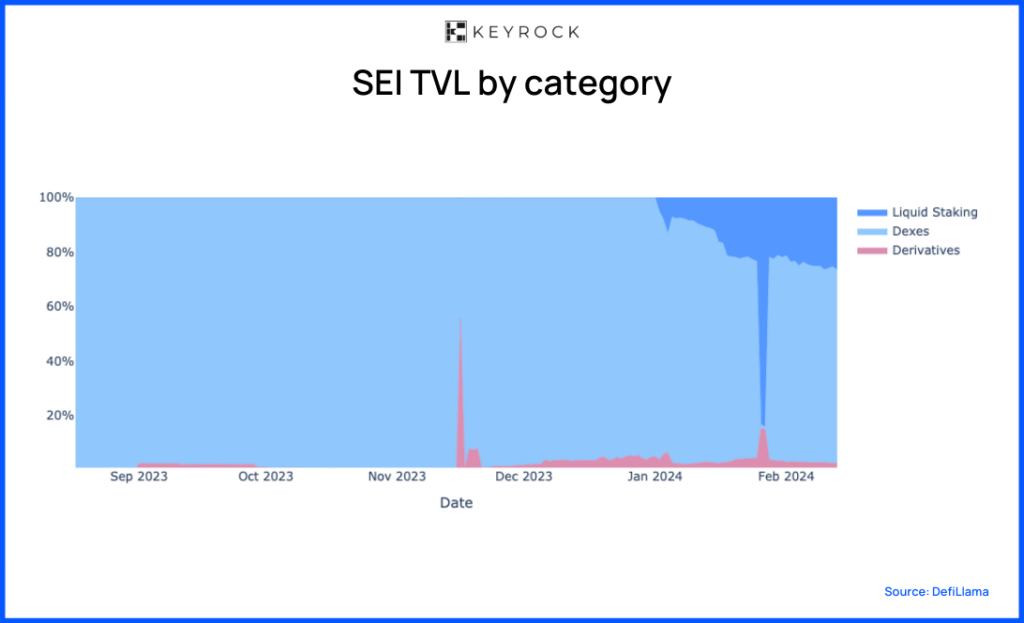

SEI – Analysis

Launching amid the bear market’s lowest point, sentiment-wise, SEI faced challenges in attracting capital. Nevertheless, it has successfully drawn $5 million in Astroport since its launch. However, breaking this initial ceiling took four months. Subsequently, SEI’s TVL quickly tripled, surpassing $15 million by the end of our snapshot.

Astroport accounted for 100% of the TVL for the first four months. The launch of liquid staking protocols, Kryptonite and SiloStake, transformed this landscape.

Note: Here, the data take into account trades which contain SEI, USDC, or USDC.eth.

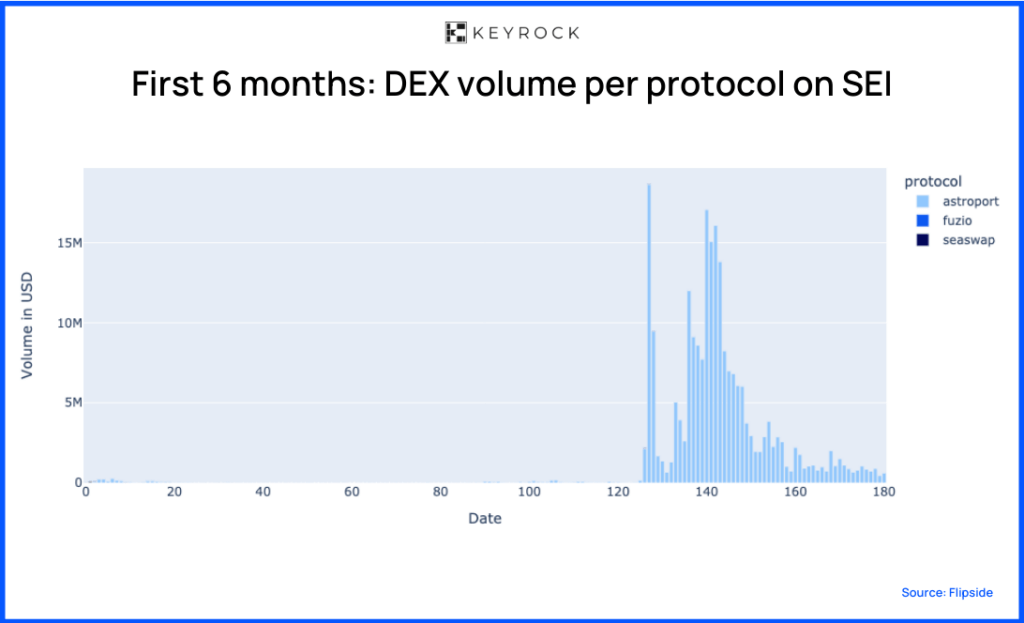

Despite a lower Total Value Locked (TVL) compared to other chains, the DEX volumes stand out, signalling robust DeFi-DEX engagement. Astroport dominates the DEX market thanks to its unrivalled liquidity. The activity remained subdued until a surge in late December 2023, when volumes peaked at $18 million.

Wrapping it up

Each chain across the board features a dominant DEX. To the point that these DEXs lead in terms of the chain’s TVL. The reason? DEXs are often the first DeFi primitive established, enabling users to swap tokens.

Following the establishment of DEXs, the subsequent development typically involves creating a money market. Beyond facilitating asset borrowing and lending, money markets also provide access to leverage. While this access may seem rudimentary, it serves its purpose until the launch of derivatives protocols.